You’ve spent months refining your product. The market is responding. The moment arrives: you need external capital terms. — but you don’t know how much to raise, from whom, or under what.

“Raising capital” is the standard expression in the startup ecosystem for securing external investment: finding investors willing to provide funding in exchange for equity.

But the key question is not just how much or when. The real question is: what needs to be true about your company for a disciplined investor to decide to back it at that specific moment?

That is the question that guides GCO Ventures, a vehicle that combines venture capital and venture building across insurance, health, home, and other sectors.

Each stage has its own logic: it’s not just the money, it’s the conversation.

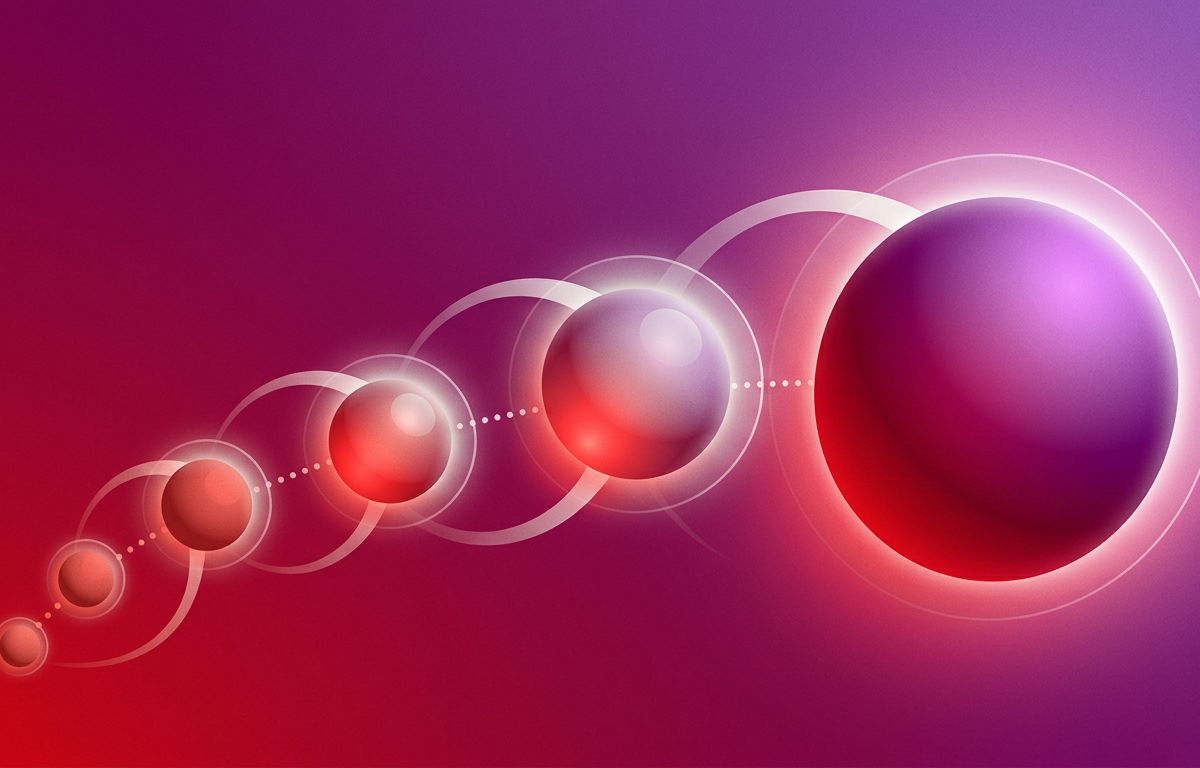

Bootstrapping is the starting point without external funding. You finance the company through your own resources, early revenues, or contributions from close contacts. You retain full control, but growth is slower.

Preseed does not fund ideas — it funds teams that have correctly identified a real problem. Typical ranges in Spain and Europe are between €50K and €500K. Investors are mainly family, friends & fools (FFF) and business angels.

The conversation at this stage revolves around one question: deeply enough to persist when our first approach fails? Do we understand the problem In regulated sectors like healthtech or insurtech, this also means demonstrating early awareness of applicable regulation. Startups that reach Preseed without identifying regulatory requirements face much tougher investor scrutiny in later rounds.

Seed consolidates what Preseed started. The typical range is €500K to €3M in Europe. You now have real users, early retention metrics, and a team of five to ten people.

At this stage, the most important signal is not growth — it is commercial learning. Investors want to see that you iterate with intent, understand why customers stay or leave, and discard hypotheses based on data. In sectors like proptech or deathtech, Seed is also when trust with traditional industry players begins to form.

In regulated industries, scaling quickly without a solid operational and regulatory foundation only builds structural risk — something investors will detect in the next round.

Series A marks the shift from exploration to execution. Typical ranges in Europe are €2M to €10M.

The conversation changes significantly: it is no longer about proving the model works under controlled conditions, but about demonstrating sustainability. Revenue must follow a pattern, teams must execute independently of founders, and metrics must support projections.

A single spike in traction is not enough in Series A — credible what investors fund is repeatability at scale.

Series B is real scaling. Typical ranges are €10M to €50M. Your company is generating several million in annual revenue and competing directly in its market.

Investors include growth equity funds and corporate VCs, who evaluate not only financial returns but also strategic fit. The focus shifts to efficiency: customer acquisition cost, lifetime value, and the ability to retain key talent.

Series C and IPO represent consolidation and exit. In Series C, rounds typically exceed €50M. Investors include large private equity funds, sovereign funds, or international strategic investors.

An IPO (Initial Public Offering) allows the company to go public and early investors to exit. Not every startup reaches this stage, nor should it necessarily aim to logic early helps make better decisions along the way.

The principle that ties it all together: how much to raise and why

The operating rule is simple: raise enough to cover 18 to 24 months of runway. In regulated sectors, add an extra 3 to 6 months. Certification processes, regulatory approvals, and negotiations with key industry players take longer than expected.

Each round implies dilution — giving up a percentage of the company. Your ownership decreases in percentage terms, even if the company’s total value increases.

Owning 20% of a €10M company is better than owning 100% of a €200K company. Dilution is not the problem — giving it up without proportional value creation is.

The type of investor also matters. A purely financial fund optimizes for returns. A corporate VC also optimizes for strategic positioning — and that has concrete implications.

At GCO Ventures, backed by Grupo Catalana Occidente, we combine venture capital with venture building. This translates into more than capital: earlystage business knowhow, strategic support, and access to a strong network of industry contacts and experti perspective differentiates us from purely financial investors.

A map doesn’t guarantee the destination — but it prevents getting lost

Understanding funding stages does not guarantee you will raise capital. It does help you understand what needs to be true about your company at each stage, what signals investors value, and what expectations to bring into the conversation.

Most failed rounds are not due to poor products — stage and targeting the wrong type of investor.

Approaching a Series A with Prethey are due to misreading the company’s seed metrics is not ambition happens too early.

If you found this article useful, you’ll find more resources on funding, key metrics, and founder strategy on the GCO Ventures blog, published monthly with the same practical approach.